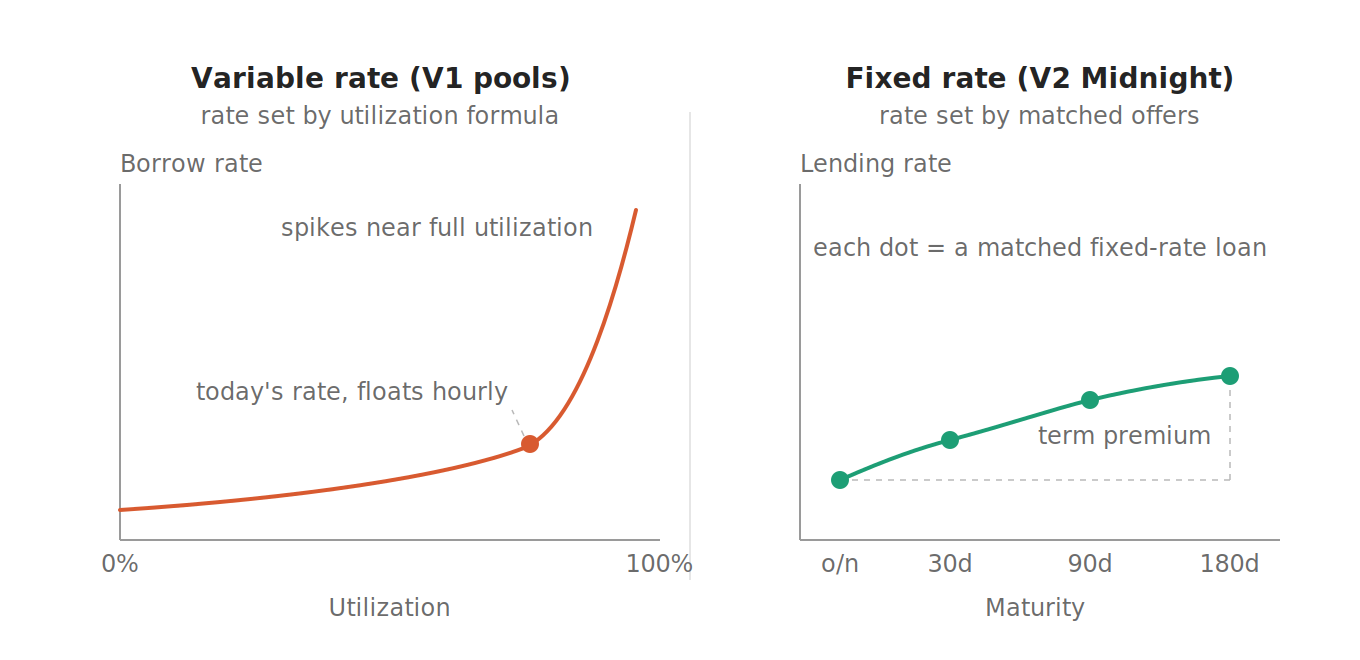

Every major lending protocol in DeFi prices credit with a lending curve formula rather than a market. Aave, Compound, Morpho Blue, Spark, Pendle etc. share the same mechanic. User deposits go into a pool, and an interest rate curve maps utilization to a certain rate. Here is how it works:

Aave sets an "optimal" utilization rate (), which is usually around 80% to 90%. The curve has two distinct slopes:

1. When (Low Demand)

Borrow rates increase gently as borrowing demand rises.

2. When (High Demand)

Borrow rates spike aggressively to prevent the pool from running dry.

The consequence is that all on-chain debt is floating rate and open term, so borrowers never know next day's funding cost, lenders never know next day's yield, and with no maturities there is no term structure and no way to price time. Morpho Midnight is the first serious attempt by a top lending protocol to fix this at the primitive level.

From pools to intents

Morpho Midnight replaces the lending curve formula with a marketplace of offers. Instead of depositing into a pool, participants express their intents. A lender offers an amount, a rate, a duration and the collateral it accepts. A borrower requests specific terms and solvers match the two sides across a single global market. Rates come from actual bids and offers rather than a governance-approved lending curve.

The same liquidity can be offered across many conditions at once, against multiple collateral types, oracles and chains, with only the matched portion drawn and the rest earning the V1 variable rate in the meantime. Collateral is equally flexible, single assets, baskets or whole portfolios, with optional KYC and whitelisting for regulated participants. The fixed rate and fixed term are the piece institutions have asked for since the first credit funds looked at DeFi, because nobody can run a balance sheet on a borrow rate that triples when utilization spikes.

Midnight is a phased rollout, half of it is live right now.

Vaults V2 shipped in September 2025, a noncustodial vaults where curators allocate deposits across any current or future Morpho protocol. Today they route mostly into V1 variable-rate markets, but their adapter architecture means that when the fixed-rate engine launches, existing vault liquidity flows into it on day one.

The fixed-rate engine itself was renamed Midnight in April 2026, with CEO Paul Frambot visioning it is a new platform running alongside Morpho Blue rather than a version update. It is not yet on mainnet, but the codebase went public in May 2026, a 400 thousand dollar audit competition, and deployment is expected once audits close. The 175 million dollar round Morpho raised in June 2026 from Paradigm, a16z crypto and Ribbit Capital at a 2 billion dollar valuation is mainly the runway for this rollout.

A fixed-term loan is also a position with defined cash flows, which means it can be sold before maturity, turning lending from a passive deposit into something closer to a bond market where credit and duration risk are priced separately. Leverage strategies change character too. The trade that dominates stablecoin DeFi today, looping a yield-bearing asset against its base asset, earns the spread between collateral yield and a floating borrow rate, and that floating leg is the main risk outside of depeg. A fixed-rate borrow converts the position into a term carry trade with a known spread to maturity, one that can finally be sized, hedged and reported the way an allocator expects

Still, every credit market in history has moved from floating, relationship-priced debt toward termed, standardized, tradable instruments. When the fixed-rate engine goes live, the interesting number will not be its TVL but the first spread between 30 day and 90 day on-chain dollars. That spread is where DeFi lending stops being a pool and starts being a market.